When it comes to parting with their hard-earned cash, consumers have a range of options to pay for goods and services: notes and coins, a few clicks on their phone, maybe an arrangement to pay a monthly fee automatically.

For some, they’ll prefer to rely on traditional methods such as cash, cheques and Standing Orders. They’re happy with the systems they use now but could be persuaded to embrace the digital revolution.

For others, they’re more interested in the different ways to pay online. They want to manage their finances quickly, efficiently and with the least disruption to their busy lives. For them, anything other than the latest tech just won’t cut it.

This also applies to you and your business. Stand still in the ever-evolving digital landscape and you’ll soon be struggling to keep pace with your competitors.

If you’re considering how your customers should be paying you, the following list of payment methods details the ins and outs and pros and cons of each: for them and for you.

There’s no one size fits all solution here. Consider your goals and objectives, your attitude to risk and your budget. Alongside this, keep your customers’ preferences and lifestyle front of mind to give them their ideal payment platform.

Read on to discover the best fit for YOUR business.

Credit and Debit Cards

Figures from UK Finance show that there are 98 million debit cards in circulation and 59 million credit cards. They’ll always be one of the most popular methods of payment.

Indeed, the volume of card payments, especially those made by debit card, is forecast to increase substantially over the next decade. Total card payment volumes are expected to rise from 14.3 billion payments in 2016 to 21.9 billion in 2026.

The total value of these is projected to reach £942 billion, up from £638 billion in 2016.

Using plastic to pay is safe and convenient, especially when customers can quickly tap their contactless card to make a purchase of up to £30. And unlike cash or cheques, if something goes wrong when paying by card, they benefit from some protection.

Cards are ideally suited to making single purchases and are a great choice of payment option for retailers, both on the high street and online.

But when it comes to using them to make and collect regular payments, the waters get a little murkier.

If you’re of a certain age, you probably remember the advertising campaign for Access, which became Mastercard in 1996, with the slogan “Your flexible friend”.

It is possible to set up your clients’ recurring payments on their credit or debit card via a Continuous Payment Authority (CPA) but the flexibility of this arrangement is questionable.

A CPA is when a customer authorises a business to withdraw money from their card repeatedly without having to ask for permission each time. Unlike Direct Debit, when the contract is with their bank, the customer has a contract with your business.

Although customers have a legal right to cancel a CPA, there are reports of some industries acting unscrupulously when it comes to playing fair. Along with this slightly tainted reputation – jeopardising your own reputation if you choose to offer them – they come with several drawbacks for businesses.

The collection cost per payment can be high, typically around 3% + 20p per payment, and failure rates are also significant at around 5%.

This is because cards expire and can be cancelled, meaning the details you hold on your database need updating regularly: an admin job your business could do without and hassle that could easily alienate your customers.

The alternative method of collecting recurring payments is to offer your customers the opportunity to pay by Direct Debit.

Direct Debit

![]()

In 2017, Direct Debit transactions experienced 3.8% growth with the number processed reaching 4.2 billion. This is 155 million more than in 2016 and has a total value of over £1.3 trillion.

Staggering statistics that reflect the popularity of the scheme: 62% of people in the UK prefer to pay regular bills by Direct Debit and nine out of 10 British adults have at least one set up. Within the health insurance industry, 63 million transactions were made, an increase of two million from 2016.

A Direct Debit is an instruction from a customer to their bank which authorises an organisation to collect payments from their account, provided they’ve given advance notice.

It allows you to reliably take regular payments from customers on a date of your choice. It’s flexible, straightforward, cost-effective and secure.

Typically used for recurring outgoings such as subscriptions, household bills and charity donations, it’s ideal for people who want the convenience of knowing their payments have been made and for businesses who want to gain control over their cash flow.

Previously only available to corporate businesses who operated Direct Debit via their sponsoring bank, it can now be used by smaller companies, organisations and charities via a specialist Bacs-approved bureau such as FastPay.

For your business, it improves cash flow, saves admin time and money, streamlines your banking, improves security and creates numerous accounting efficiencies.

For your customers, it gives them peace of mind, convenience, flexibility and control. They know that their payments are being made on the right date and that they won’t be faced with late payment charges or a disruption to your service.

They’re also protected by the Direct Debit Guarantee, giving them total reassurance thanks to its safeguards. These include an immediate money back guarantee from their bank if a debit is made in error, and the right to cancel a Direct Debit at any time if they let you and their bank know.

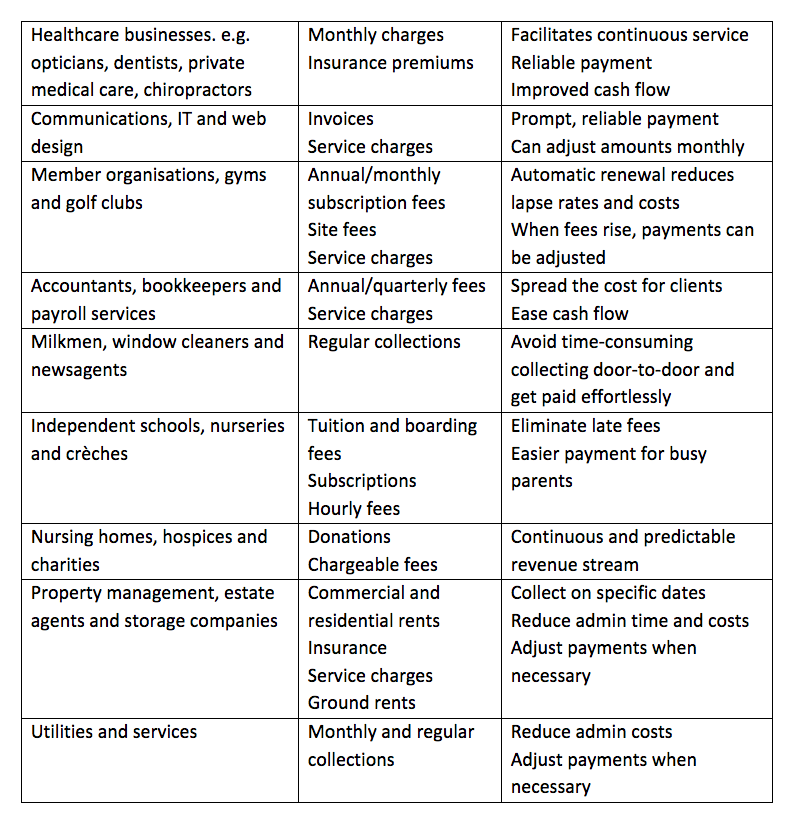

The table below shows Direct Debit’s versatility across a range of sectors, along with specific benefits:

Direct Debit’s adaptability to meet business needs compared to other methods of payment is clear to see. For the private healthcare industry, it means monthly income from regular premiums will arrive predictably in your account.

You’ll also benefit from regular reports informing you of the status of all Direct Debit payments, including cancellations and rare failures, so you’re equipped with a real-time overview of your account.

Other Forms of Electronic Payment

If your business model suits accepting payments over the internet, then there are several different ways to pay online.

The most prevalent is the Faster Payments scheme which offers 24/7 near real-time payments between 25 UK banks and building societies. It allows electronic payments to be made online, over the phone, in-branch or through self-service kiosks.

It’s a speedy system with transactions typically clearing within two hours and acts as the default service for all internet and mobile banking activity.

With over nine billion Faster Payments made since it launched in 2008, they are perfectly suited to making payments such as bills, online purchases and transfers, and supplier invoices.

Faster Payments figures for May 2018 show a 19% year-on-year increase in the number of processed payments to 167.3 million. These payments totalled £140 billion, a 21% increase from May 2016. And in 2017, there were 230 million more payments than in 2016: an increase of 16%.

Mobile wallets, such as Apple Pay, Google Pay and Samsung Pay, are also growing in popularity among ways to pay online. These apps allow customers to simply use their smartphone to pay you in person using a compatible merchant card reader.

For your private healthcare business, carefully consider the type of services you’ll be charging for and the model you’ll be following. These ways to pay online are suitable for one-off sales and service invoices: you’ll see the money in your account straightaway and your customers will appreciate the convenience.

But if you need to charge fees on a regular basis, their limitations will create headaches through extra admin and a lack of reporting.

Standing Orders

Before Direct Debit soared in popularity, the go-to method to make regular payments was via Standing Orders. These are instructions from a customer to their bank to pay a fixed amount to a business on a regular basis.

They’re ideal when paying for predictable outgoings such as rent and magazine subscriptions or when transferring cash to a savings account.

But problems can arise when a business wants to alter the amount it charges its customers. For example, if you want to increase monthly premiums, the onus would be on your client to change their Standing Order set-up.

This is because any changes to the amount, frequency or date of collection must be arranged by your customer with their bank. Unlike Direct Debit, when the ball is in your court and you can adapt payments to suit your business needs, Standing Orders put the customer in control.

They can cancel or change a Standing Order without informing you: you’ll only discover what they’ve done when the payment doesn’t appear. This could take a month or longer, depending on the payment frequency.

Your cash flow is then unexpectedly compromised and, rather than a payment on the expected date, you get an unwelcome surprise when you check your account.

For businesses, their usefulness is restricted in terms of flexibility and reliability.

For your customers, they can create more admin for them if you request changes and they offer less consumer protection than a Direct Debit.

Cash and Cheques

In the 350 years since the first cheque was recorded, this most traditional of payment methods has reached the dizzy heights of popularity and the rock bottom lows of near oblivion.

Two years after plans were announced in 2009 to discontinue the cheque clearing system, it won a reprieve and pulled itself back from the brink.

For now, cheques are clinging on obstinately, despite falling numbers year-on-year. Latest statistics from the Cheque and Credit Clearing Company show that they processed 15% fewer cheques in 2017 than in 2016: 293 million compared to 344 million.

And the value of these has decreased from £400m to £356m, an 11% drop which although still a significant sum shows that surely the cheque’s days are numbered.

For your business, the drawbacks of accepting cheques from customers are numerous: they can bounce, they require manual reconciliation and a physical visit to a bank or ATM to cash, they can arrive late, if at all, and they could also take around 5-6 days to clear.

The latter of these potential issues could see some improvement with the gradual introduction of the Image Clearing System. This will speed up the clearance process by allowing banks to exchange images of cheques rather than the physical cheque itself.

After its full roll-out is complete in late 2018, cheques will clear much quicker than the current paper system, eliminating some of the uncertainty and delay involved.

Funds will leave a payer’s account and arrive in the payee’s account by 23.59 the next working day.

Think carefully about whether you want to offer cheques as one of your methods of payment. Improvements are being made but figures show that only 55% of UK personal account holders said that they’d either made or received a payment by cheque in the past year. This compares to 90% of UK adults who have at least one Direct Debit commitment and 77% of people who think positively about Direct Debit.

Like cheques, cash is the most admin-heavy in our list of payment methods, with the added risk of being lost, stolen or even counterfeit.

Now you know all about the methods of payment available to your business, you can make an informed decision on which will best suit your needs; whether that’s making the ease and convenience of Direct Debit the only option for your customers or offering a combination of alternatives.

Consider the pros and cons of each carefully and, with a robust and relevant payment system in place, look forward to your business powering forward.