When it comes to making and taking payments, it appears that there are no shortage of options (or acronyms) for transferring funds. Choosing a payment method that works for your particular set of circumstances can be an unenviable task, with the added pressure of bank fees or time constraints often looming in the background. In this article, we examine two of the most popular bank-to-bank payment transfer methods – Bacs and CHAPS. We’ll talk you through the what, why and how of each option so that you can make an informed decision.

Bacs vs CHAPS Quick Navigation

What are Bacs and CHAPS payments?

![]()

Let’s start with some definitions.

Bacs payment meaning

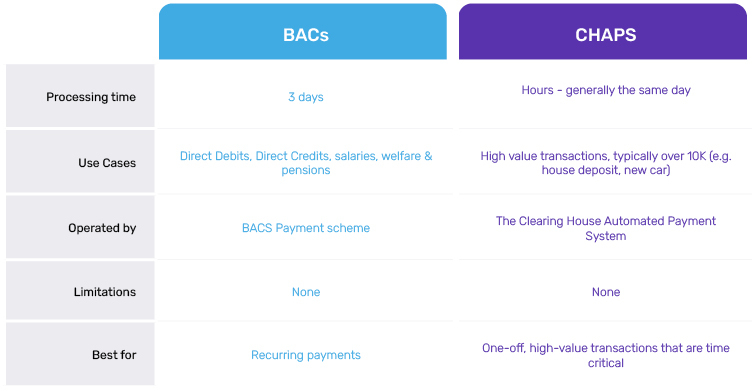

Bacs is short for Bankers Automated Clearing System and is a common way to send money electronically between banks. Bacs payments typically fall into one of two camps – Direct Debits where money is taken from an account as per the Direct Debit instruction and Direct Credit Payments; where money is paid out into an account such as in the cases of salaries, pensions and welfare payments. An average of 100 million transactions per day are made possible by Bacs transfers.

What is a CHAPS payment?

CHAPS is the abbreviated form of Clearing House Automated Payment System. This is another common bank-to-bank payment system but it is typically reserved for large, one-off payments. To add some context, CHAPS turns over the annual UK GDP every six days. The CHAPS all time peak value day was recorded on 18th March 2020 when some £479 billion was settled by this payment method alone.

What’s the difference between Bacs and CHAPS?

If both Bacs and CHAPS are automated, bank-to-bank payment systems, how do you know which one is best for you? The answer to this question lies in a consideration of two major factors: the size of the transaction and speed.

For large, one-off transactions such as a house deposit or a new car purchase, CHAPS is often the preferred payment method. With no upper limit on how much can be transferred and offering same day processing and clearing (subject to strict time cut-offs), CHAPS is ideal for those big ticket, time-critical purchases.

By comparison, Bacs payments take 3 working days to clear. On day one, the payments are submitted to Bacs; day two they are processed by the banks and on day three, payment is taken from the sender and credited to the recipient simultaneously.

However, this does not mean that Bacs Direct Debits should be discounted for one-off transactions. Yes, Bacs is a “set and forget” method that is favoured for taking or making regular payments but it is also incredibly flexible. Direct Debits can, and are, used for occasional payments where same day clearing is not required. Direct Debit has the added benefit of protecting customers from fraudulent payments or payments made in error via the Bacs guarantee.

Bacs or CHAPS infographic

To summarise, the differences between Bacs and CHAPS are illustrated in the chart below:

How much do Bacs and CHAPS cost?

Another consideration in the Bacs Vs CHAPS debate is cost.

Bacs payments either by Direct Debit or Direct Credit are one of the cheapest ways to transfer funds between banks. But a few words of caution: if you are setting up a Direct Debit yourself to collect payments, be prepared to incur some initial outlay. Obtaining Bacs approved software and a SUN (Service User Number) can be time consuming and costly.

That’s why many businesses, organisations and clubs trust Direct Debit providers such as FastPay Ltd to collect on their behalf. As a Bacs approved bureau and Bacs affiliate, the team here at FastPay can get you set up and collecting within 24 hours. Outsource your payment collections to us and we’ll take care of it all – no need to source software, a SUN or get tied into ongoing technical support fees. We do it all whilst you stay in charge. And our pricing? We believe in offering a transparent, affordable service with prices from 3p per transaction.

Compare this cost to the £25 – £30 bank charge that is typically applied to CHAPS payments.

What about Faster Payments?

![]()

A closely related cousin of Bacs and CHAPS payments is the Faster Payments (FP) Scheme. This is a relatively new payment system that allows electronic payments to be processed quickly, in near real-time. Completed over the phone, online or in-branch, Faster Payments were responsible for over 2.4 billion payments in 2019.

Said to rival the speed of CHAPS payments and offering the convenience of paying a mobile number rather than a bank account, Faster Payments are mainly used for small value payments. Use cases include bills, supplier invoices and online transfers.

However, Faster Payments are restricted by an upper limit of £250,000 per transaction and can be open to user error. Once a Faster Payment is sent, it cannot be cancelled meaning that any mistakes will result in the permanent loss of those funds. Furthermore, not all banks and building societies (at present) are signed up to the service.

Take control of your Bacs payments with FastPay

Bacs, CHAPS or Faster Payments, managing your cash flow doesn’t have to be hard. For those who want to be in control of when they get paid, Bacs Direct Debits offer a cost-effective solution where same day payment is not necessary. By automating your recurring or one-off collections with Direct Debit, you can get paid on time, automatically.

Let FastPay help you find your Direct Debit solution by calling 0161 737 5290.

Alternatively, you can request our latest brochure or get a quote by completing our quick contact form.