The word “Bacs” is likely to make many people instantly think of payday: over 361 million payroll transactions were processed via the Bacs payment system in 2016.

It appears on millions of UK bank statements as the transfer method for monthly pay and you’ll probably be familiar with it from your own personal accounts.

But beyond the payroll, how else can you use Bacs within your business and how does it compare to other types of payment? How do you set up a Bacs scheme and what methods can it replace and improve upon?

This comprehensive guide to Bacs payment services will explain all you need to know.

TABLE OF CONTENTS

- What is a Bacs payment

- The Bacs Payment System: Direct Debit and Bacs Credit

- Faster Payments

- Standing Orders

- CHAPS

- Cheques

- How Do Businesses Use Bacs Payments?

- How Do You Set Up a Bacs Payment System?

- How Much Do Bacs Payments Cost?

What is a Bacs payment?

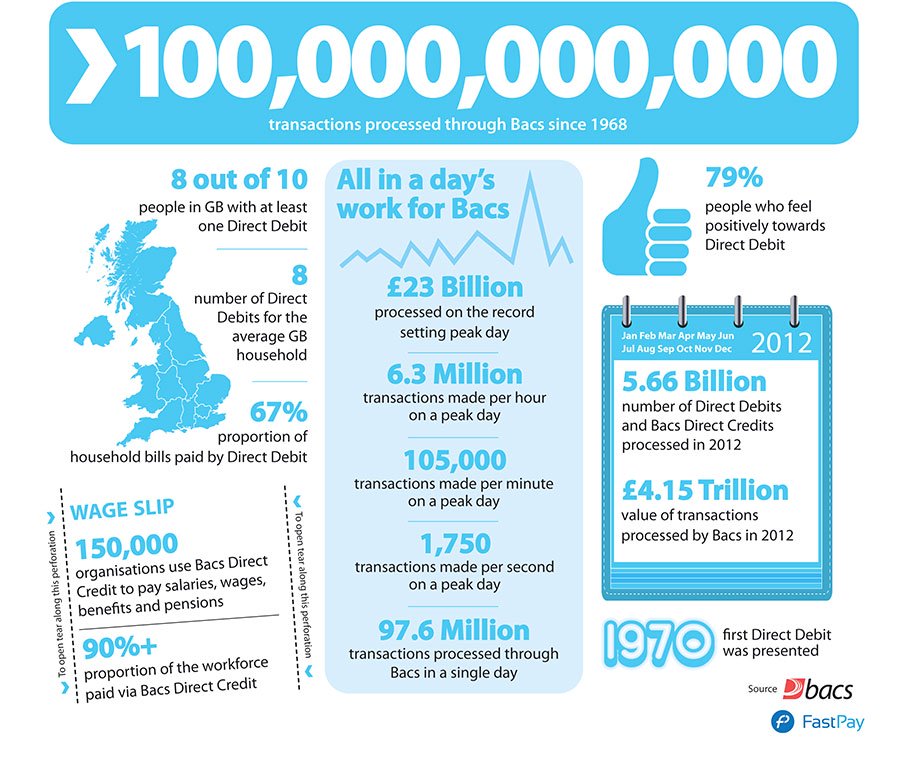

Well, firstly some stats:

Bacs is a system which allows the electronic transfer of funds between UK banks. It was established in 1968, two years after the first credit card was launched and three years before decimalisation.

Bacs is a system which allows the electronic transfer of funds between UK banks. It was established in 1968, two years after the first credit card was launched and three years before decimalisation.

Almost 50 years on, it now processes billions of transactions each year in the form of Direct Debits and Bacs Direct Credits. These payments are fully automated to simplify moving money from one account to another on a regular basis.

From collecting membership fees and monthly payment instalments to paying pensions and benefits, they offer businesses and organisations an efficient, streamlined option to manage their credit control and accounting.

The popularity of Bacs payment services shows no sign of slowing down. In 2016, 11 new processing records were set, including:

- A 3% increase in the total number of transactions processed to 6.222 billion.

- A 4.9% increase in the number of Direct Debits processed to 4.07 billion.

- A 4.1% increase in the value of Direct Debits processed to £1.26 trillion.

- A 4.9% increase in the value of Direct Credits processed to £3.52 trillion.

- A 5% increase in the highest number of transactions processed in one day to 109.3 million. This record was broken on 30th June 2017 when 111.7 million transactions took place.

Since its inception, more than 120 billion transactions have been debited or credited to British bank accounts via Bacs.

You could play a part in the next set of stats by incorporating Bacs payments into your business strategy. If you’re currently relying on outdated payment methods such as cheques or Standing Orders, automating your accounting systems will bring your business fully into the digital age.

The Bacs Payment System: Direct Debit and Bacs Direct Credit

Direct Debit is an instruction from a customer to their bank which authorises an organisation to collect payments from their account, provided they’ve given advance notice.

Direct Debit is an instruction from a customer to their bank which authorises an organisation to collect payments from their account, provided they’ve given advance notice.

It allows you to take regular payments from customers on a date of your choice. It’s flexible, straightforward, cost-effective and secure.

Typically used for recurring outgoings such as subscriptions, household bills and charity donations, it’s ideal for people who want the convenience of knowing their payments have been made.

Previously only an option for large, corporate businesses who operated Direct Debit via their sponsoring bank, it can now be used by smaller companies, organisations and charities via a specialist Bacs-approved bureau such as FastPay.

2016 stats from Bacs show the total volume of Direct Debits processed in several different sectors. For example:

- Life insurance 161 million

- Charity donations 108 million

- Gym subscriptions 50 million

- Club/society/professional membership 12 million

Almost nine out of 10 British adults have at least one Direct Debit with 73% of household bills paid via the Bacs scheme. A further 62% prefer to pay regular bills by Direct Debit.

![]() Bacs Direct Credit is a safe and simple way for businesses and organisations to transfer money directly into another bank or building society account.

Bacs Direct Credit is a safe and simple way for businesses and organisations to transfer money directly into another bank or building society account.

It allows you to make regular payments to people on a date of your choice.

Commonly known as a bank transfer, it’s most often used to pay wages, salaries and state benefits. It’s also the preferred payment method for pension payments, employee expenses, insurance settlements and tax credits.

Almost 90% of the UK workforce is paid by Bacs Direct Credit and one billion benefit payments are made this way each year.

Unlike cash or cheques, Bacs Direct Credit payments cannot be lost, stolen or delayed in the post. They’re an affordable, flexible and reliable means of moving money.

The 2016 Bacs stats show that 2.15 billion Direct Credit transactions were made in total, with payroll making up 361m of this figure, private pensions 83m, state pensions 323m and Child Benefit 158m.

Now you know the answer to the question “What is a Bacs payment?”, what other money transfer options are available to your business?

Faster Payments

![]() The Faster Payments scheme offers near real-time payments between 10 UK banks and building societies.

The Faster Payments scheme offers near real-time payments between 10 UK banks and building societies.

Launched in 2008, it allows electronic payments to be made online, over the phone, in-branch or through self-service kiosks. Five billion payments have been made since it began.

Faster Payments usually clear within two hours and are best suited to making large numbers of smaller payments such as bills, online purchases and transfers, and supplier invoices.

Its popularity is growing: the latest figures, which are updated monthly, show a 13% year-on-year increase in the number of processed payments in September 2017 to 138.7 million. These payments totalled £118 billion, a 16% increase from September 2016. And in 2016, there were 179 million more payments than in 2015: an increase of 14%.

However, despite their speed and convenience, Faster Payments are restricted to a maximum of £250,000, with some banks imposing a lower transaction limit.

And if one of the banks or building societies at either end of the transaction isn’t on board with Faster Payments, it will automatically transfer to Bacs Direct Credit which will have a longer processing time.

They’re also not designed to efficiently manage taking payments from customers, unlike Direct Debit which, provides unrivalled benefits.

Standing Orders

A Standing Order is an instruction from a customer to their bank to pay a fixed amount to you on a regular basis. Any changes to the amount, frequency or date of collection must be arranged by your customer with their bank.

A Standing Order is an instruction from a customer to their bank to pay a fixed amount to you on a regular basis. Any changes to the amount, frequency or date of collection must be arranged by your customer with their bank.

With Direct Debit, the ball is in your court. You adapt the payment to suit your business needs, putting you in complete control.

With Standing Orders, the customer is in control. They can cancel or change a Standing Order without informing you: you’ll only discover what they’ve done when the payment doesn’t show up. This could take a month or longer, depending on the payment frequency.

Your cashflow is then unknowingly compromised and, rather than a payment on the expected date, you get a nasty surprise.

Standing Orders only work efficiently for regular, fixed payments such as rent or transferring cash to a savings account. Their inflexibility becomes more obvious when it comes to variable payments for other personal expenses such as credit card and utility bills.

For businesses, a standing orders usefulness is limited compared to the flexibility of Direct Debit.

CHAPS

![]() The Clearing House Automated Payment System (CHAPS) manages high-value bank-to-bank transfers when same day guaranteed payment is required.

The Clearing House Automated Payment System (CHAPS) manages high-value bank-to-bank transfers when same day guaranteed payment is required.

Launched in 1984, there’s no limit to how much money can be sent via CHAPS although with fees of around £35 per transaction, it is an expensive option.

You may have used CHAPS when buying or selling a house or car but it’s mainly used for wholesale transactions of sterling between banks and building societies

In fact, CHAPS transfers by individual home buyers and sellers, and solicitors and conveyancers overseeing house sales, accounts for less than 1% of the trillions of pounds processed each year.

The scale of the CHAPS system is impressive:

- It turns over the equivalent of the UK’s GDP every six days

- In July 2011, the total value of money processed since CHAPS began exceeded one quadrillion

And as a fast and secure method of transferring high sums, its popularity continues to grow:

- In 2016, the total value of CHAPS payments grew by 10.5% year-on-year to a record £75.6 trillion, an average of £299 billion every day

- In September 2017, CHAPS processed 3.4 million payments worth £7.1 trillion over 21 settlement processing days

- The average daily value for the month was £339 billion, an increase of 12.9% from September 2016

For SMEs, charities and small organisations, CHAPS isn’t a suitable or affordable money transfer method due to the high values involved and the processing fees.

FastPay have put together a handy guide exploring the CHAPS vs Bacs debate.

Cheques

The first UK cheque was issued in 1659. If you’re still relying on a 350-year-old method to collect customer payments, it’s definitely time to consider a more modern alternative.

The first UK cheque was issued in 1659. If you’re still relying on a 350-year-old method to collect customer payments, it’s definitely time to consider a more modern alternative.

At the peak of the cheque’s popularity in 1990, over 4 billion were processed that year. But these days, cheque books are more likely to be found languishing in drawers than carried around daily in bags and briefcases.

Major high street names including Boots, Asda and Next no longer accept them and some banks offer incentives to new customers for not requesting a cheque book.

Statistics from the Cheque and Credit Clearing Company show that they processed 15% fewer cheques in 2016 than in 2015: 344 million compared to 404 million.

The value of these has decreased from £454m to £400m, a 12% drop which, although not as dramatic as some had predicted, is still significant.

For businesses, the drawbacks of the cheque are obvious: they can easily bounce, they take a long time to clear, they require time-consuming reconciliation and they often arrive late, if at all.

In summary, if your business is looking to make automatic payments, you have a choice of three systems: Bacs Direct Credit, Faster Payments and CHAPS.

If your business is looking to take automatic payments, Direct Debit via Bacs is your strongest option.

How Do Businesses Use Bacs Payments?

Bacs payment services are ideally suited to many business payment purposes. From salaries to subscriptions and service charges to site fees, Direct Debit and Bacs Direct Credit are highly flexible, reliable and secure.

Bacs Direct Credit is the perfect solution to making regular payments to employees and suppliers: automated, hassle-free and straightforward. Over 150,000 businesses use the system to pay salaries, pensions, expenses and invoices. It’s also used by the Department for Work and Pensions to pay millions of pounds in benefits.

Direct Debit is used to collect money from customers regularly and reliably. For your business, it improves cashflow, saves admin time and money, streamlines your banking, improves security and creates numerous accounting efficiencies.

For your customers, it gives them peace of mind, convenience, flexibility and control. They know that their payments are being made on the right date and that they won’t be faced with late payment charges.

They’re also protected by the Direct Debit Guarantee, giving them total reassurance thanks to its safeguards. These include an immediate money back guarantee from their bank if a debit is made in error, and the right to cancel a Direct Debit at any time if they let you and their bank know.

The table below shows Direct Debit’s versatility across a range of sectors, along with specific benefits:

| INDUSTRY | TYPE OF PAYMENT | BENEFITS |

| Communications, IT and web design | Invoices Service charges |

Prompt, reliable payment Can adjust amounts monthly |

| Member organisations, gyms and golf clubs | Annual/monthly subscription fees Site fees Service charges |

Automatic renewal reduces lapse rates and costs When fees rise, payments can be adjusted |

| Accountants, bookkeepers and payroll services | Annual/quarterly fees Service charges |

Spread the cost for clients Ease cash flow |

| Milkmen, window cleaners and newsagents | Regular collections | Avoid time-consuming collecting door-to-door and get paid effortlessly |

| Independent schools, nurseries and crèches | Tuition and boarding fees Subscriptions Hourly fees |

Eliminate late fees Easier payment for busy parents |

| Nursing homes, hospices and charities | Donations Chargeable fees |

Continuous and predictable revenue stream |

| Property management, estate agents and storage companies | Commercial and residential rents Insurance Service charges Ground rents |

Collect on specific dates Reduce admin time and costs Adjust payments when necessary |

| Utilities and services | Monthly and regular collections | Reduce admin costs Adjust payments when necessary |

Direct Debit’s adaptability to meet numerous business payment needs is clear to see. Whether you’re a sole trader, SME, charity or school, Direct Debit will bring clear benefits to your accounting team and wider business.

How Do You Set Up a Bacs Payment System?

There are two main ways to access Direct Debit: managing the process in-house and working directly with your bank, or signing up with a Direct Debit company who can do the job for you.

The first, direct access option is only feasible if you’re a large organisation with a high turnover. For some banks, this needs to be at least £1m. This figure will immediately exclude numerous businesses.

If you meet this basic criterion and are accepted by your bank, be aware that setting up a direct scheme can be a long process and costs can be prohibitive. You will also need to ensure you have the necessary technical expertise and most up-to-date Bacs-approved software within your business to manage Direct Debits professionally.

The second option is to take advantage of a Direct Debit facility which does everything for you, such as FastPay. They’ll offer you expert advice on what will work best for your business.

A Direct Debit bureau usually offers two distinct schemes: a bureau service for corporate businesses with their own Service User Number (SUN) from a bank and a facilities management (FM) service for SMEs, charities and organisations for those who can’t get a SUN.

Each service makes it easy to collect Direct Debit payments from customers: a time-effective, cost-effective and simple solution for your business.If you want to set up Bacs Direct Credit to pay your employees, this is only possible through a Bureau Service with your own SUN number.

Once you’re signed up to a bureau such as FastPay, your Bacs payment services will be up and running within just 24 hours, immediately empowering you and your business.

In order to accept Direct Debit payments, you’ll need a Service User Number (SUN) – a unique code given to each organisation which collects money via the scheme.

In order to accept Direct Debit payments, you’ll need a Service User Number (SUN) – a unique code given to each organisation which collects money via the scheme.

Bacs uses SUNs as a form of ID to keep a record of all corresponding transactions. It’s also used by banks to look up the name of the company to be included on the payers’ bank statements.

If you sign up as a bureau client, you’ll already have your own bank-sponsored SUN. To acquire one of these, your company must prove its management expertise, financial health and contractual capacity.

This approval allows you to either manage Direct Debits in-house or outsource to one of the Direct Debit providers, enjoying lower processing fees.

For businesses unable to meet the banks’ strict requirements, you’ll be provided with an SUN by your Direct Debit company which will enable you to start collecting payments straightaway via a facilities management, or managed, service.

This frees you from the onerous task of gaining your bank’s approval and paying their high set-up fees.

FastPay uses unique SUNs for each Managed Service client, meaning that your business name and logo, rather than the impersonal name of your bureau, will appear on all documents including bank statements.

Armed with your SUN, you can now tell your customers that you’re switching to Bacs payment services. They’ll soon be enjoying peace of mind, convenience, flexibility and control over their budget: a more efficient service for them and you.

Each customer will need to complete, sign and return a Direct Debit Instruction authorising you to collect payments from them, provided you give advance notice. This can be done either online, over the phone or on paper.

Direct Debit providers can supply branded Bacs-approved web forms, phone scripts and paper mandates to gather all the information you need such as account numbers and sort codes, payment amounts and collection dates.

They will also manage the submission of this data to Bacs on your behalf. Your customers’ accounts will then be debited and payments transferred into your business account once they’ve cleared (or on the same day if use a bureau service, rather than an FM one).

How Much Do Bacs Payments Cost?

Setting up as a direct submitter to your bank can be a costly way of accessing the power of Bacs payments. Managing Direct Debits in-house requires an initial outlay of many thousands of pounds on set-up fees, Bacs-approved software and staff training. The ongoing fees and workload will also be high.

Setting up as a direct submitter to your bank can be a costly way of accessing the power of Bacs payments. Managing Direct Debits in-house requires an initial outlay of many thousands of pounds on set-up fees, Bacs-approved software and staff training. The ongoing fees and workload will also be high.

Deciding to become an indirect submitter and outsourcing to a bureau is a more affordable option. You’ll still pay a set-up fee and be charged per collection, but the costs are easily recouped through a significant reduction in admin hours.

FastPay has a transparent, competitive pricing structure which makes business budgeting easy. There are no monthly or annual fees and volume discounts are available.

For a Managed Service, set-up fees are as little as £175 with each Direct Debit transaction costing between 10p-50p depending on volume.

For a Bureau Service, set-up fees are no more than £375 with each Direct Debit and Bacs Direct Credit costing as little as 3p.

In addition, you receive free phone and email support, and fees are invoiced separately rather than deducted from each individual collection to simplify reconciliation.

Choose FastPay for Leading Payment Solutions

What is a Bacs payment? Now you know, it’s clear that using Direct Debit or Bacs Direct Credit in your business will give other payment methods a run for their money.

Find out more why you should choose FastPay when it comes to direct debit.